Stablecoins are growing faster than credit cards not because of hype, but because they solve structural problems in modern payments. From instant settlement and lower fees to global accessibility and programmable money, stablecoins fit today’s digital economy in ways legacy card networks cannot. This article explores the real economic, behavioral, and technological forces driving stablecoin adoption—and why traditional payment systems are struggling to keep pace.

Introduction: Why the Payment System Americans Rely on Is Quietly Being Challenged

For decades, credit cards have been the default engine of consumer payments in the United States. They shaped how Americans shop, travel, subscribe, and borrow. Swipe, tap, earn rewards, repeat—it became muscle memory.

Yet beneath that familiarity, cracks are forming.

Merchants complain about rising fees. Global businesses struggle with cross-border friction. Freelancers wait days—or weeks—to get paid. Digital platforms need faster settlement to survive. Consumers expect money to move as fast as information.

Into this environment stepped stablecoins—a form of digital money designed not to speculate, but to move value efficiently.

Their rapid growth isn’t an accident. It’s a signal that the financial system is being forced to evolve.

What Are Stablecoins, Explained Simply

Stablecoins are digital currencies designed to maintain a stable value, usually pegged 1:1 to the U.S. dollar.

Unlike traditional cryptocurrencies, stablecoins aim to function as:

- Digital cash

- Settlement tools

- Payment infrastructure

They allow users to send, receive, and store dollar-equivalent value without relying on traditional card networks or bank clearing systems.

In practice, stablecoins behave less like investments and more like programmable dollars.

Are Stablecoins Actually Growing Faster Than Credit Cards?

In consumer retail, credit cards still dominate. But growth rates tell a different story.

Stablecoins are expanding far more rapidly in:

- Cross-border payments

- Freelance and creator economies

- Business-to-business settlements

- Digital platforms and marketplaces

- Emerging and underserved markets

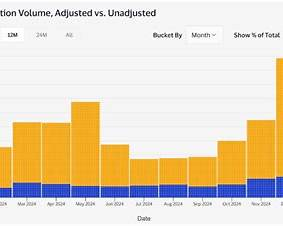

Blockchain analytics consistently show trillions of dollars in annual stablecoin transaction volume, with year-over-year growth that outpaces traditional card usage in many segments.

This growth isn’t theoretical—it’s operational.

The Real Reason #1: Settlement Speed Is No Longer Optional

Credit cards feel instant, but the money doesn’t actually move right away.

Behind every card transaction:

- Funds pass through multiple intermediaries

- Merchants wait days for settlement

- Chargebacks can reverse payments weeks later

Stablecoins settle transactions near-instantly, often within minutes.

For businesses, this changes everything:

- Faster access to cash

- Improved liquidity

- Lower working capital needs

- Simpler reconciliation

In a digital economy, time equals money, and stablecoins save both.

The Real Reason #2: Credit Cards Break Down Outside U.S. Borders

Credit cards were built for domestic commerce.

The moment payments go global, problems appear:

- Foreign transaction fees

- Currency conversion costs

- Declined transactions

- Delayed settlement

Stablecoins ignore borders entirely.

They allow:

- Dollar-denominated payments anywhere

- Consistent fees regardless of geography

- Faster payouts to global workers

- Reduced dependency on local banks

For remote teams and international platforms, stablecoins often feel like the first payment system designed for how the internet actually works.

Real-Life Example: Paying Global Freelancers

A U.S. company hiring a developer overseas typically faces:

- Wire transfer fees

- Banking delays

- Currency loss

- Administrative overhead

With stablecoins:

- Payment arrives in minutes

- Fees are minimal

- Value remains dollar-pegged

- The freelancer controls when and how to convert funds

The appeal isn’t ideological—it’s practical.

The Real Reason #3: Merchant Fees Are Eating Into Profits

Credit card payments come with layered costs:

- Interchange fees

- Network assessments

- Processor margins

For many merchants, total costs reach 2–4% per transaction.

Stablecoin payments can significantly reduce those expenses by:

- Eliminating intermediaries

- Automating settlement

- Reducing fraud exposure

As profit margins tighten, businesses naturally gravitate toward cheaper rails.

The Real Reason #4: Chargebacks Are a Hidden Liability

Chargebacks are a major pain point for merchants.

They lead to:

- Revenue loss

- Operational complexity

- Fraud vulnerability

- Unpredictable cash flow

Stablecoin transactions are typically final.

That finality:

- Reduces fraud

- Simplifies accounting

- Improves certainty for sellers

For digital goods, subscriptions, and creator platforms, this is a major advantage.

The Real Reason #5: Programmable Money Beats Static Cards

Credit cards move money—but they don’t think.

Stablecoins can be programmed to:

- Release funds automatically

- Enable escrow arrangements

- Power subscriptions

- Trigger payments on conditions

This enables new business models that credit cards struggle to support.

In a software-driven economy, money that behaves like software scales faster.

Are Stablecoins Replacing Credit Cards?

No—and that’s an important distinction.

Stablecoins are not replacing cards at grocery stores or restaurants overnight.

Instead, they are:

- Replacing wires

- Competing with ACH

- Challenging cross-border card dominance

- Powering backend settlement layers

Credit cards remain consumer-facing tools. Stablecoins are becoming financial infrastructure.

Why Most Consumers Don’t Even Notice Stablecoins

Many people use stablecoins without realizing it.

They encounter them through:

- Fintech apps

- Digital wallets

- Payment platforms

- Backend settlement systems

Because stablecoins often operate invisibly, adoption accelerates without friction.

Just as users don’t think about internet protocols, they increasingly won’t think about payment rails.

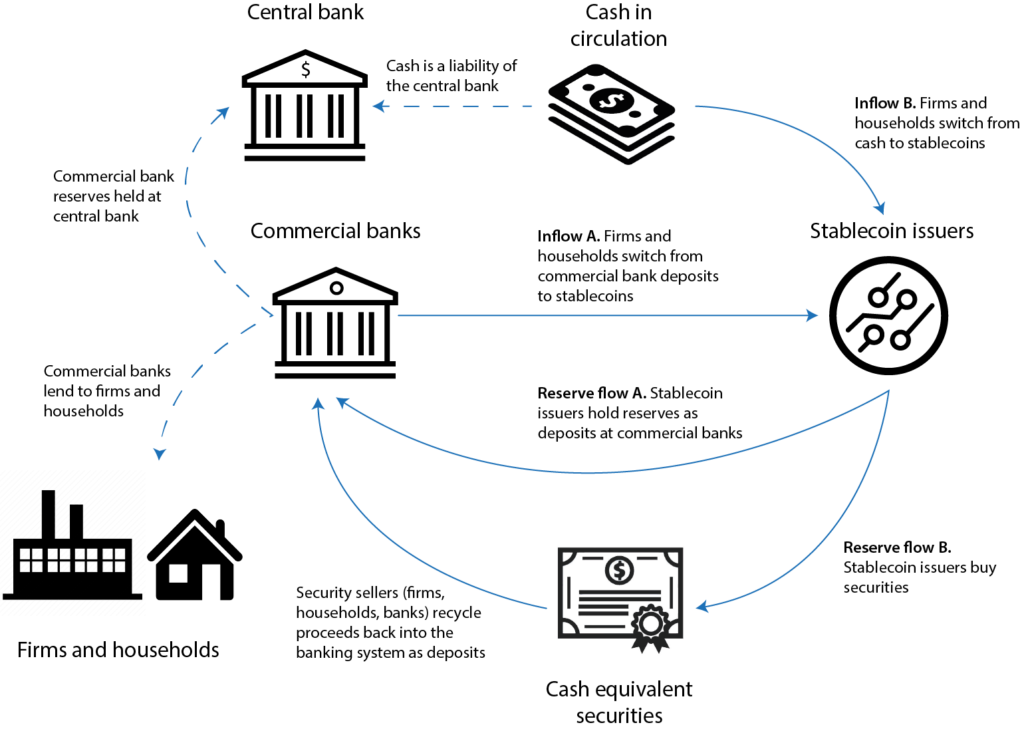

The Trust Factor: Why People Use Stablecoins Anyway

Trust doesn’t come from technology alone—it comes from reliability.

People trust stablecoins because:

- They hold value consistently

- They settle quickly

- They work globally

- They reduce friction

Ironically, stablecoins succeed because they don’t feel experimental.

What About Regulation?

Regulation is increasing, not disappearing.

U.S. policymakers are focusing on:

- Reserve transparency

- Consumer protection

- Compliance standards

Clearer rules may actually accelerate adoption by:

- Reducing uncertainty

- Encouraging institutional use

- Standardizing best practices

History shows that payments grow fastest once regulation stabilizes.

Pain Points Stablecoins Solve That Credit Cards Cannot

- Slow settlement

- High merchant fees

- Cross-border friction

- Chargeback abuse

- Limited programmability

Stablecoins are not perfect—but they solve problems cards were never designed to address.

Practical Takeaways for Businesses and Consumers

For businesses:

- Explore stablecoins for international payments

- Use them for B2B settlement

- Start with pilot programs

For consumers:

- Treat stablecoins as payment tools, not investments

- Use regulated platforms

- Focus on usability and security

The Bigger Shift: Payments Are Becoming Invisible Infrastructure

Credit cards are products.

Stablecoins are plumbing.

As commerce becomes global, digital, and always-on, the systems that move money must adapt accordingly.

Stablecoins are growing because they fit that future better.

Final Thought: This Growth Isn’t About Crypto—It’s About Efficiency

Stablecoins aren’t winning because of hype.

They’re winning because:

- Money needs to move faster

- Costs need to come down

- Borders need to matter less

Credit cards defined payments in the 20th century.

Stablecoins are quietly redefining them in the 21st.

Frequently Asked Questions (10 SEO-Optimized FAQs)

1. Why are stablecoins growing faster than credit cards?

They offer faster settlement, lower fees, and better global usability.

2. Are stablecoins safer than credit cards?

They reduce some risks but require careful platform selection.

3. Can stablecoins be used for everyday purchases?

Increasingly yes, especially online and cross-border.

4. Are stablecoins legal in the U.S.?

Yes, though regulatory frameworks continue to evolve.

5. Do stablecoins replace banks?

No. They complement and modernize banking infrastructure.

6. Why do businesses prefer stablecoins?

Speed, cost efficiency, and programmability.

7. Are stablecoins volatile?

They are designed to maintain stable value.

8. Will credit cards disappear?

Unlikely—but their dominance may gradually decline.

9. Who benefits most from stablecoins?

Freelancers, global businesses, and digital platforms.

10. Are stablecoins the future of payments?

They are likely a core component of future payment systems.