The Federal Reserve is often viewed as the most powerful force in global finance, but markets increasingly challenge its authority. Bond yields, stock prices, and investor expectations frequently push the Fed to react rather than lead. This article explores the modern power struggle between the Fed and financial markets, explaining who truly shapes interest rates, inflation, and economic outcomes today.

Introduction: The Quiet Power Struggle Shaping the Economy

For generations, investors followed one simple rule: “Don’t fight the Fed.”

The belief was clear—when the Federal Reserve sets policy, markets eventually fall in line.

But recent years have exposed a more complicated reality.

Markets now regularly front-run, challenge, and sometimes force reversals in Federal Reserve policy. Bond yields move against official guidance. Stocks rally despite tightening. Financial conditions loosen even as the Fed tries to slow the economy.

This raises a fundamental question Americans are increasingly asking:

Is the Federal Reserve still in control, or have markets taken over?

The answer matters more than most people realize. It affects mortgage rates, retirement accounts, job security, inflation, and the cost of everyday life.

What the Federal Reserve Is Designed to Control

The Federal Reserve’s mandate has remained largely unchanged for decades:

- Price stability (controlling inflation)

- Maximum employment

- Financial system stability

To achieve this, the Fed relies on several core tools:

- Adjusting short-term interest rates

- Expanding or shrinking its balance sheet

- Providing liquidity during financial stress

- Communicating future policy intentions

In theory, these tools give the Fed immense power. In practice, their effectiveness depends on how markets respond.

How Markets Act as a Counterweight to the Fed

Markets are not passive. They continuously assess risk, future growth, inflation expectations, and policy credibility.

Through trillions of daily transactions, markets influence:

- Long-term interest rates

- Mortgage and loan costs

- Corporate financing conditions

- Asset prices

- Consumer and business confidence

When markets move in a direction the Fed doesn’t want, policymakers are often forced to respond—whether they admit it or not.

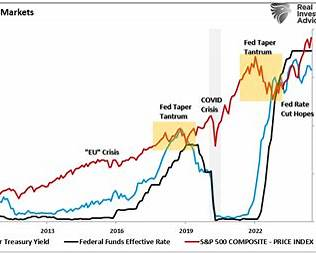

Real-World Example: The 2018 Policy Reversal

In 2018, the Fed raised interest rates and reduced its balance sheet, signaling confidence in economic strength. Markets disagreed.

Stocks fell nearly 20% in a matter of weeks. Credit spreads widened. Financial conditions tightened sharply.

By early 2019, the Fed reversed course, pausing rate hikes and signaling patience.

The takeaway was unmistakable: markets forced the Fed to pivot.

Who Actually Controls Interest Rates?

This is where the Fed’s power is often misunderstood.

The Fed controls overnight and short-term interest rates.

Markets control long-term interest rates.

Mortgage rates, auto loans, and corporate borrowing costs depend largely on long-term Treasury yields—set by investors, not policymakers.

When the Bond Market Pushes Back

There have been many periods when:

- The Fed cut rates, but mortgage rates rose

- The Fed promised hikes, but yields fell

- Markets priced future rate cuts long before the Fed acknowledged them

These moments reveal a critical truth: the bond market often leads, and the Fed follows.

Inflation: The Ultimate Test of Control

Inflation has become the clearest battleground between the Fed and markets.

Despite aggressive rate hikes in recent years:

- Housing costs remained elevated

- Service inflation stayed persistent

- Wage pressures continued

- Inflation expectations fluctuated

Markets frequently priced in future rate cuts while the Fed insisted inflation was not yet defeated. This gap created volatility across assets.

Inflation revealed the Fed’s limits—especially in a world shaped by supply chains, demographics, and global shocks.

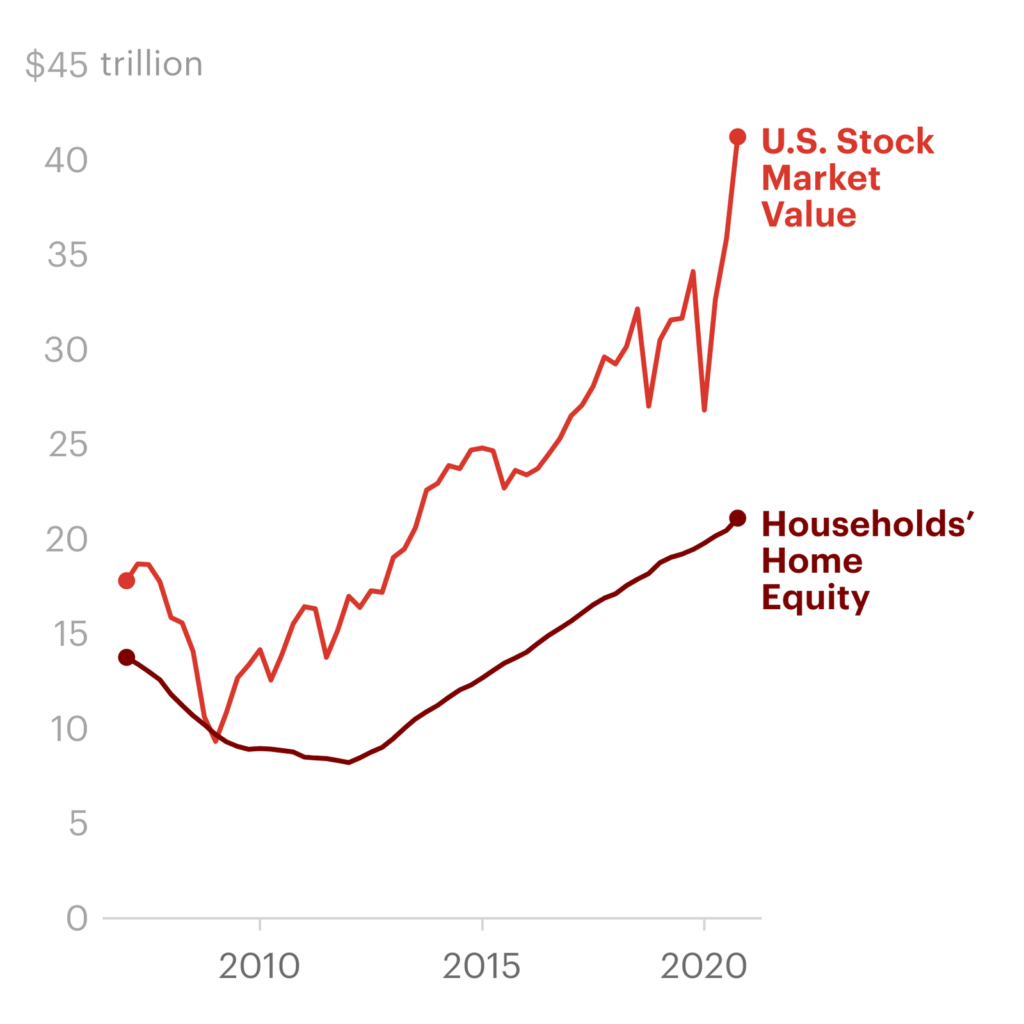

The Stock Market’s Influence on Policy Decisions

While the Fed does not officially target stock prices, market declines carry real consequences:

- Reduced consumer spending

- Slower business investment

- Job losses

- Political pressure

Sharp market sell-offs often trigger softer policy language or emergency interventions.

The “Fed Put” Effect

Many investors believe the Fed will step in if markets fall too far. This belief encourages risk-taking and speculation, which ironically makes it harder for the Fed to tighten policy without destabilizing markets.

In this way, market expectations actively shape Fed behavior.

Why Fed Communication Has Become So Powerful

In modern markets, words often matter more than actions.

Investors analyze:

- Press conference tone

- Small wording changes

- Economic projections

- Individual Fed official speeches

A single phrase can move trillions of dollars in minutes.

However, reliance on communication creates fragility. If credibility weakens, markets stop responding the way policymakers expect.

Global Forces Further Reduce Fed Control

The Fed operates in a global financial system, not a closed economy.

Global influences include:

- Foreign central bank policies

- Capital flows into and out of the U.S.

- Currency movements

- Geopolitical risks

- Energy and commodity shocks

For example, strong global demand for U.S. Treasuries can push yields lower even when the Fed wants tighter conditions.

So, Who’s Really in Control?

The honest answer is uncomfortable but realistic:

Control shifts constantly.

- During crises, the Fed often regains authority

- During expansions, markets assert dominance

- In periods of uncertainty, influence swings back and forth

Rather than absolute control, the modern system operates through feedback loops.

What This Means for Everyday Americans

You don’t need to trade markets to feel this power struggle.

Real-Life Impacts Include:

- Mortgage rates moving independently of Fed decisions

- Retirement accounts reacting to expectations, not policy

- Job markets weakening despite rate cuts

- Savings yields changing unpredictably

Understanding this dynamic helps households plan more realistically.

Practical Guidance for Investors and Families

Instead of trying to predict Fed decisions, focus on resilience.

Smart Financial Principles Today:

- Diversify across assets and income sources

- Avoid excessive debt

- Maintain emergency savings

- Focus on long-term fundamentals

- Ignore short-term policy noise

In today’s economy, adaptability is more valuable than certainty.

Frequently Asked Questions (SEO-Optimized)

1. Does the Federal Reserve control the stock market?

No. It influences conditions, but markets often move independently.

2. Who controls long-term interest rates?

The bond market primarily determines long-term rates.

3. Why do markets sometimes ignore the Fed?

Because investors price future risks differently than policymakers.

4. What is the “Fed put”?

The belief that the Fed will intervene if markets fall sharply.

5. Can markets force the Fed to change policy?

Indirectly, yes—through financial conditions and economic impact.

6. Does the Fed fully control inflation?

No. Global forces, wages, and supply chains also matter.

7. Why is Fed communication so important?

Because expectations shape spending and investment behavior.

8. Are markets more powerful than the Fed today?

At times, especially in long-term pricing.

9. Should investors trust Fed guidance?

As one input, not as a guarantee.

10. What matters more: policy or psychology?

In the short term, psychology often dominates.

Final Thoughts: Influence Has Replaced Control

The idea that the Federal Reserve fully controls markets is outdated.

Today’s financial system is shaped by constant interaction between policymakers and investors. Each reacts to the other. Each tests limits.

The Fed still matters enormously—but it no longer acts alone.

For investors, households, and decision-makers, the most important insight is this:

Understanding the Fed-market power struggle is no longer optional—it’s essential.