A new generation of crypto-fintech partnerships is reshaping U.S. mortgage lending by blending blockchain efficiency with regulated financial institutions. These collaborations promise faster approvals, lower costs, improved transparency, and better access for underserved borrowers—without requiring consumers to use cryptocurrency. If widely adopted, they could modernize one of America’s most outdated financial processes.

Introduction: Why Mortgage Lending Still Feels Broken

For many Americans, applying for a mortgage is not just stressful—it feels outdated. Despite living in a world of instant payments, real-time banking alerts, and one-click financial apps, buying a home still involves weeks of document collection, repetitive verification requests, unclear fees, and constant uncertainty.

The average borrower uploads the same pay stubs, bank statements, and tax returns multiple times to different systems. Even small discrepancies can delay approvals. Closing dates shift. Costs rise. Trust erodes.

This is precisely why a new crypto-fintech partnership model is drawing attention across the housing, banking, and regulatory landscape. Rather than replacing the mortgage system, these partnerships aim to upgrade its core infrastructure, quietly modernizing how loans are verified, approved, closed, and serviced.

And unlike earlier crypto hype cycles, this shift is grounded in real-world financial pain points Americans experience every day.

What Is This New Crypto-Fintech Partnership?

At its core, this model pairs blockchain technology providers with regulated fintech companies or licensed mortgage lenders. Each side focuses on what it does best.

- The crypto or blockchain firm supplies secure digital infrastructure, smart contracts, and automated verification tools.

- The fintech or lender handles compliance, underwriting, customer service, loan servicing, and regulatory obligations.

This division of labor is crucial. It ensures innovation happens within existing financial rules, rather than outside them.

Importantly, borrowers usually interact with a familiar mortgage platform—not a crypto exchange. Blockchain works in the background, improving speed and transparency without adding complexity.

Why Is This Happening Now?

Mortgage Inefficiency Has Become Too Expensive to Ignore

Industry research estimates that U.S. mortgage origination costs often exceed $8,000 per loan, driven largely by manual labor, fragmented data systems, and compliance overhead. These costs ultimately show up in higher fees for borrowers.

Blockchain-based automation offers lenders a way to cut costs without sacrificing compliance.

Regulatory Attitudes Have Matured

Regulators today distinguish between speculative crypto trading and infrastructure-level blockchain use. Technologies that enhance auditability, reduce fraud, and improve consumer transparency are increasingly viewed as tools—not threats.

Consumer Expectations Have Changed

Americans can open bank accounts, invest in stocks, and send money instantly. Waiting 30–45 days for a mortgage decision feels increasingly unreasonable. The pressure to modernize is coming directly from consumers.

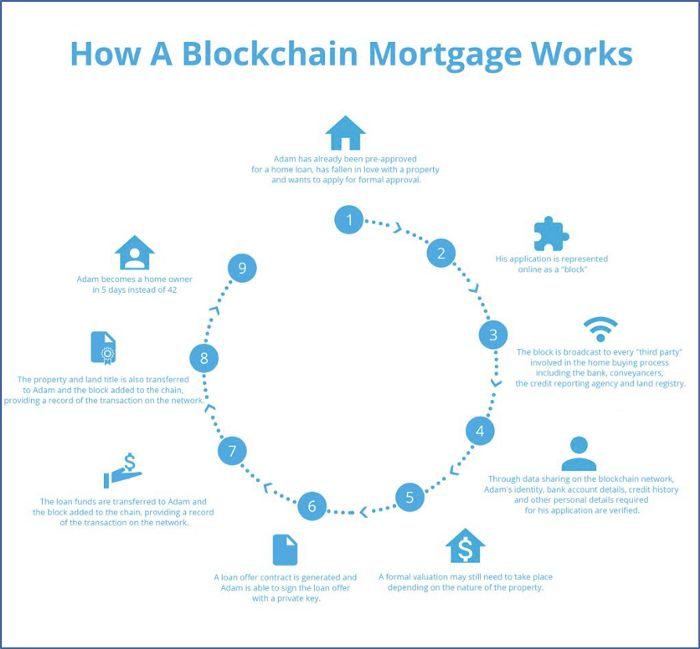

How Blockchain Changes the Mortgage Process

Faster Verification and Underwriting

Verification is one of the biggest bottlenecks in mortgage lending. Blockchain allows verified financial data—such as income history or asset balances—to be securely shared across approved parties.

Instead of repeatedly uploading documents, borrowers authorize access once. This reduces errors, speeds approvals, and minimizes human intervention.

Automated Escrow and Settlement

Smart contracts can automate escrow conditions, release funds when requirements are met, and log every step immutably. This reduces delays caused by manual checks and miscommunication between third parties.

Real-Time Transparency for Borrowers

A blockchain-based ledger provides a shared, tamper-resistant record of loan progress. Borrowers can see where their application stands, what’s pending, and who is responsible—reducing anxiety and confusion.

Clearing Up a Common Misconception: This Is Not a “Bitcoin Mortgage”

One of the most searched questions online is whether borrowers need cryptocurrency to use these systems.

The answer is no.

Most crypto-fintech mortgage partnerships:

- Use blockchain as infrastructure

- Keep loans denominated in U.S. dollars

- Follow traditional lending and servicing rules

Borrowers may never interact with crypto assets at all.

Real-Life Scenarios Where This Matters

The Self-Employed Borrower

Freelancers and small business owners often struggle to prove stable income. Blockchain-based financial records can create verifiable, time-stamped income histories that reduce underwriter uncertainty.

The First-Time Homebuyer

For buyers already overwhelmed by down payments and interest rates, faster approvals and clearer fees can make the difference between winning or losing a home.

The Remote or Cross-Border Worker

As remote work grows, traditional underwriting struggles with international income. Secure digital verification systems can simplify assessments without increasing risk.

Why Banks and Large Lenders Are Paying Attention

Large banks once viewed crypto innovation as a threat. That mindset has shifted.

Today, banks face:

- Fintech lenders offering faster approvals

- Rising consumer expectations

- Pressure to reduce operational costs

Crypto-fintech partnerships offer a way to modernize without ripping out legacy systems.

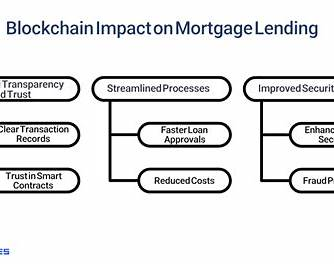

Key Benefits Driving Adoption

While still emerging, these partnerships offer clear advantages:

- Reduced approval timelines

- Lower origination and closing costs

- Improved fraud detection

- Enhanced borrower trust through transparency

- Better access for non-traditional borrowers

These are structural improvements, not cosmetic ones.

Risks and Challenges That Remain

Regulatory Complexity

Mortgage lending is heavily regulated. Any technology used must comply with federal, state, and consumer protection laws. Missteps could slow adoption.

Consumer Perception

Many Americans still associate crypto with volatility and scams. Clear communication and branding matter.

Integration with Legacy Systems

Mortgage platforms are complex. Poorly executed integration could create new bottlenecks instead of removing old ones.

How Regulators Are Likely to Respond

Regulators tend to support innovations that:

- Improve transparency

- Strengthen audit trails

- Protect consumers

As long as crypto-fintech partnerships remain compliant and consumer-focused, regulatory resistance is likely to be cautious rather than prohibitive.

What This Means for the Future of Homeownership

If adoption continues, these partnerships could:

- Shorten the homebuying timeline

- Reduce borrower stress

- Expand access to credit

- Lower systemic costs across the industry

In a housing market where affordability and speed are critical, even incremental improvements can have a massive impact.

Practical Takeaways for Homebuyers

- You don’t need crypto to benefit from blockchain-backed mortgages

- Faster approvals may soon become standard

- Transparency around fees and timelines is likely to improve

The biggest change may not be visible—but it will be felt.

Frequently Asked Questions (10 FAQs)

1. What is a crypto-fintech mortgage partnership?

It’s a collaboration where blockchain firms provide infrastructure while regulated lenders handle mortgages.

2. Do I need to own cryptocurrency to apply?

No. Most systems operate entirely in U.S. dollars.

3. Are these mortgages legal in the United States?

Yes, when structured within existing lending regulations.

4. Can blockchain really speed up mortgage approvals?

Yes. Automation and secure data sharing can significantly reduce delays.

5. Are crypto-backed mortgage systems safe?

When properly implemented, they can improve security and auditability.

6. Will interest rates be lower?

Rates depend on the market, but operational savings may reduce fees.

7. Are banks being replaced?

No. Most models involve collaboration, not replacement.

8. Is this technology already in use?

Yes. Pilot programs and early implementations are underway.

9. Does this help first-time homebuyers?

Yes, through clearer costs, faster approvals, and reduced friction.

10. What should borrowers be cautious about?

Always verify lender licensing, disclosures, and consumer protections.

Final Thoughts: A Quiet but Powerful Shift

This new crypto-fintech partnership trend isn’t about speculation—it’s about infrastructure. By modernizing processes Americans have complained about for decades, it has the potential to transform mortgage lending in practical, meaningful ways.

The future of homebuying may not look radically different—but it will feel faster, clearer, and fairer.