Rising Federal Reserve interest rates are putting millions of Americans at risk of higher car payments, tighter credit approval, and growing financial stress. Auto loan delinquencies are surging as lenders respond to Fed policy shifts with stricter standards and higher APRs. This in-depth guide explains how Fed decisions directly impact your car loan—and what steps you can take to protect your finances before the next policy move.

Introduction

For years, most Americans rarely thought about the Federal Reserve when shopping for a car. But all of that has changed. As interest rates climbed at the fastest pace in decades, millions of consumers began feeling the squeeze—not just in mortgages, but in one of the most essential forms of consumer credit: auto loans.

Car loans have quietly become the next major financial pain point for households. With rates at multi-decade highs, vehicle prices still elevated, income growth falling behind inflation, and lenders turning more cautious, the humble car loan now sits at the center of a growing affordability crisis. Economists warn that auto loans may be the next major casualty of shifting Fed policy, and the effects are already showing up in rising delinquencies and shrinking credit access.

But how does Fed policy directly affect car loan costs? Why are lenders tightening standards? Who is most vulnerable? And how can you protect yourself before the next economic shift?

This comprehensive blog answers all of these questions—using real-life examples, current data, and search-based insights to help you understand what’s happening and what to do about it.

How Fed Policy Directly Impacts Your Car Loan

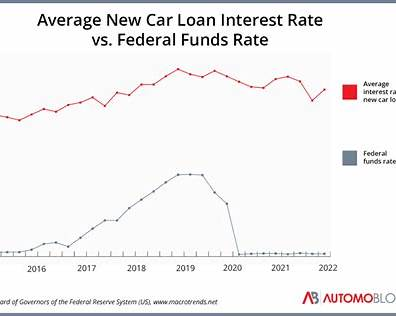

Many consumers mistakenly believe that the Federal Reserve controls only mortgage rates. In reality, the Fed influences almost every major credit market, including auto loans.

When the Fed raises interest rates:

- Banks face higher borrowing costs

- Lenders pass those costs to consumers

- Auto loan APRs rise

- Monthly payments increase

- Lenders tighten their approval criteria

The result? A car that was affordable two years ago now costs dramatically more to finance.

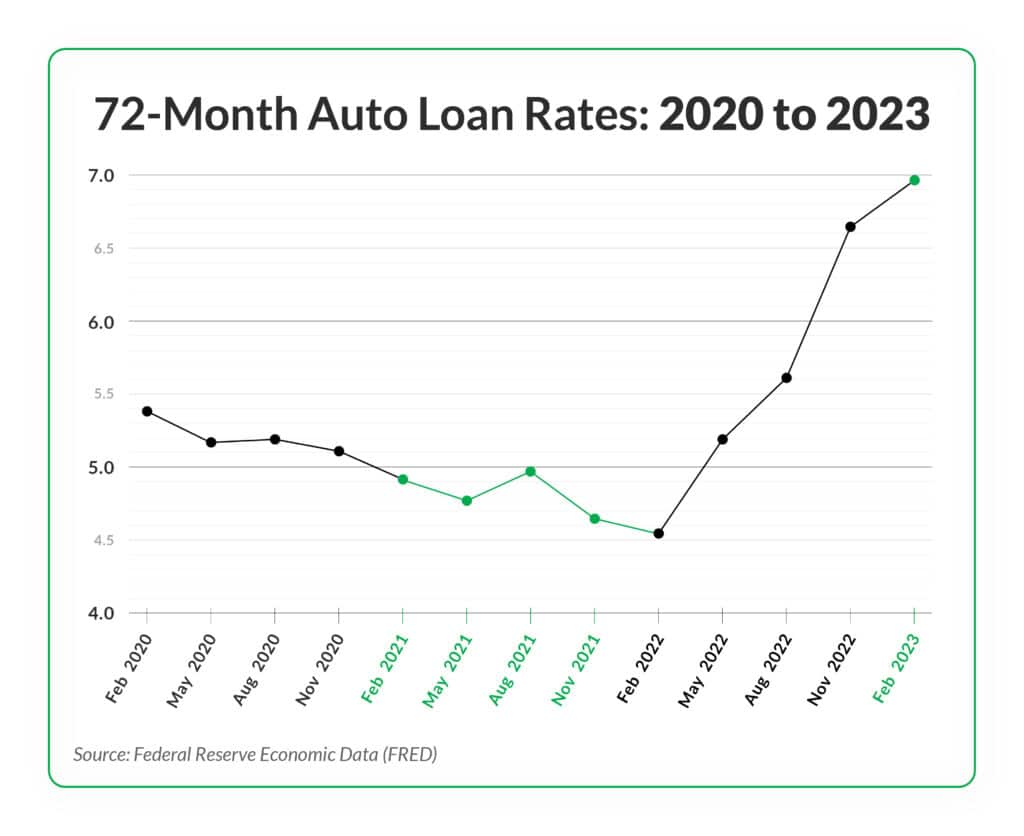

According to data from the New York Federal Reserve, by late 2024:

- The average new-car loan rate exceeded 9.8%

- Used car loan rates climbed to 14%

- Subprime borrowers saw APRs above 20–27%

This is the most expensive auto-financing environment in more than two decades.

Real-Life Example

A couple in Tennessee attempted to finance a 4-year-old Toyota RAV4. Despite stable income and a 690 credit score, the lowest rate they were offered was 14.5%—more than double what they could have secured before the Fed began tightening rates. Their monthly payment ended up nearly $200 higher than expected.

Why Auto Loans Are Becoming the Weak Link in the Economy

Several economic forces are converging to make auto loans especially vulnerable to Fed policy shifts:

1. Persistently High Car Prices

Both new and used vehicles remain significantly more expensive than before the pandemic.

- New cars average $47,000

- Used cars remain 35–40% higher than pre-2020 levels

Even if interest rates stabilized, high vehicle prices alone would still pressure affordability.

2. High Interest Rates Compound the Problem

When rates go up, monthly payments increase dramatically. For example:

A $35,000 loan at 3.9% APR → ~$645/month

The same loan at 11.9% APR → ~$810/month

That difference—$165/month—can break a household budget already strained by inflation.

3. Stagnant Wage Growth

While expenses climbed, wage growth slowed in 2024–2025. This means more Americans are stretching their budgets thinner than ever before.

4. Banks Are Getting More Conservative

As delinquencies rise, lenders tighten standards to protect themselves. This creates a feedback loop:

Higher rates → fewer approvals → more desperate buyers → more delinquencies → even tighter lending.

5. Longer Loan Terms = Higher Risk

Many Americans are resorting to 72–84 month loans to make payments manageable. This leads to:

- Negative equity for years

- Higher repossession risk

- Bigger losses for lenders

Why Your Car Loan May Be the Next Casualty

Below are the primary reasons analysts warn the auto loan sector is poised for trouble.

1. Higher Rates Are Pricing Out Millions of Buyers

When APRs reach double digits, even modest vehicles become unaffordable.

Real-Life Example

A single mother in Phoenix found that her pre-approved car loan from 2021 would have been $310/month for a used Toyota Camry. In 2024, after rate hikes, the updated quote was $475/month—a price jump that forced her to walk away.

2. Lenders Are Tightening Credit Standards

Banks now require:

- Bigger down payments

- Higher credit scores

- Lower debt-to-income ratios

- More employment documentation

This disproportionately affects middle-income families, young drivers, and anyone with imperfect credit.

3. People Who Bought Cars in 2021–2023 Are Underwater

Many buyers financed vehicles at peak pandemic prices. Now that values have dropped, millions owe more than their cars are worth. According to Edmunds, 22% of trade-ins involve negative equity, averaging $5,500.

4. Delinquencies Are Rising Fast

Auto loan delinquencies are now at their highest since 2010.

Young borrowers (ages 18–29) are struggling the most, with nearly 9% behind on payments.

5. A Credit Crunch Could Hit the Auto Market Hard

If lenders pull back even further, car sales may slow, repossessions could rise, and manufacturers may face production cuts—echoes of previous economic downturns.

Will Car Loan Rates Drop If the Fed Cuts Rates?

Possibly—but not immediately, and not for everyone.

Even when the Fed cuts rates:

- Lenders may lower APRs slowly

- Subprime borrowers may see little relief

- Auto prices could rise again if demand increases

- Only borrowers with strong credit will benefit meaningfully

Analysts predict that even after cuts, auto loan rates may stay above pre-2020 levels for several years.

Who Is Most at Risk Right Now?

Data from Experian and TransUnion reveals the following groups face the highest danger:

1. Subprime Borrowers

APR often exceeds 20%.

2. Buyers With High Debt-to-Income Ratios

Any household spending more than 15–20% of its take-home pay on a vehicle is vulnerable.

3. Recent Buyers With High Negative Equity

Those who purchased during peak pricing (2021–2023).

4. Young Borrowers

Lower wages + limited credit history = higher APRs.

5. Gig Workers and Delivery Drivers

High mileage accelerates depreciation and maintenance costs.

How to Know If Your Car Loan Is at Risk

Watch for these warning signs:

- Your payment exceeds 15% of your take-home income

- You need to refinance just to stay current

- You owe $3,000+ more than the car is worth

- Insurance costs make your total monthly burden unsustainable

- You’re delaying maintenance to afford payments

If two or more apply—you’re in the high-risk zone.

How to Protect Yourself Before the Next Fed Policy Shift

Here are practical, actionable steps (with a mix of paragraph and pointers):

1. Check Your Equity Position Immediately

Knowing whether you’re underwater helps you avoid costly mistakes, like trading in a vehicle too early or rolling debt into a new loan. Use KBB, Edmunds, or Carvana to check your car’s value against your loan balance.

2. Consider Refinancing When Rates Fall

Refinancing works best if:

- Your credit score improves

- Your income stabilizes

- Your car retains its value

Borrowers with good credit can reduce their APR by several percentage points.

3. Make a Principal-Only Extra Payment

A one-time payment of even $300–$500 can reduce interest substantially, especially early in the loan.

4. Improve Your Credit Before Financing Again

Key credit-boosting steps:

- Reduce credit card utilization below 30%

- Remove outdated or incorrect credit report entries

- Avoid new inquiries before applying

- Keep older accounts open

A 60-point credit improvement can cut your APR significantly.

5. Shop Beyond Dealership Financing

Dealers often mark up APRs. Instead, check:

- Credit unions

- Online lenders

- Local community banks

They frequently offer lower rates and more flexible underwriting.

6. Choose the Shortest Affordable Loan Term

A 60-month term typically offers the best balance of affordability and long-term protection against negative equity.

7. Avoid Unnecessary Add-Ons

Extended warranties, GAP, tire packages, and service plans can add $1,500–$4,000 to your loan. Only choose what you truly need.

What to Do If You Can’t Afford Payments Anymore

Instead of waiting for repossession:

• Contact Your Lender Early

Most offer hardship programs, payment deferrals, or loan modifications.

• Sell the Vehicle Before It’s Repossessed

Private sales usually generate far better value than auction prices.

• Downsize to a More Affordable Car

This is often the most financially effective solution.

• Temporarily Shift to Public Transit or Car-Sharing

A short-term lifestyle adjustment can stabilize long-term finances.

10 Frequently Asked Questions About Fed Policy & Auto Loans

1. Will auto loan rates drop in 2025 or 2026?

Possibly, if the Fed cuts rates. But lenders may reduce APRs slowly and selectively. Rates may remain above pre-pandemic averages.

2. Why are auto loan delinquencies rising?

High prices, high interest rates, and slower wage growth are pushing borrowers past their limits.

3. Can I refinance my car loan?

Yes—especially if your credit score improved or if rates fall. But refinancing won’t help much if you’re deeply underwater.

4. Do Fed decisions directly change car loan rates?

Not instantly, but they strongly influence the rates lenders set because those are tied to benchmark rates controlled by the Fed.

5. Why are used cars still expensive?

Inventory shortages, inflation, reduced fleet sales, and strong demand for budget-friendly vehicles.

6. Should I buy a car now or wait?

If you can wait, you may save money as rates drop. But supply constraints could raise prices in some segments.

7. Are young adults affected more than older buyers?

Yes. Younger borrowers usually have lower income and thinner credit profiles, leading to higher APRs.

8. Is there an auto loan bubble?

Not like housing, but rising negative equity and delinquencies show instability.

9. How long will high car prices last?

Analysts expect elevated prices into 2025–2026, especially for used vehicles.

10. What is the safest loan term today?

Most experts recommend 48–60 months to avoid long-term negative equity and excessive interest.

Final Thoughts: Prepare Before Fed Policy Hits Your Wallet

Car loans may be the next major financial casualty of Federal Reserve policy shifts. Whether you’re planning to buy a car, refinance an existing loan, or simply survive rising economic uncertainty, understanding how Fed decisions impact auto financing is essential.

By getting ahead of rate movements, improving your credit, and choosing smarter loan structures, you can shield yourself from sudden financial shocks—and avoid becoming one of the millions trapped in unaffordable vehicle debt.